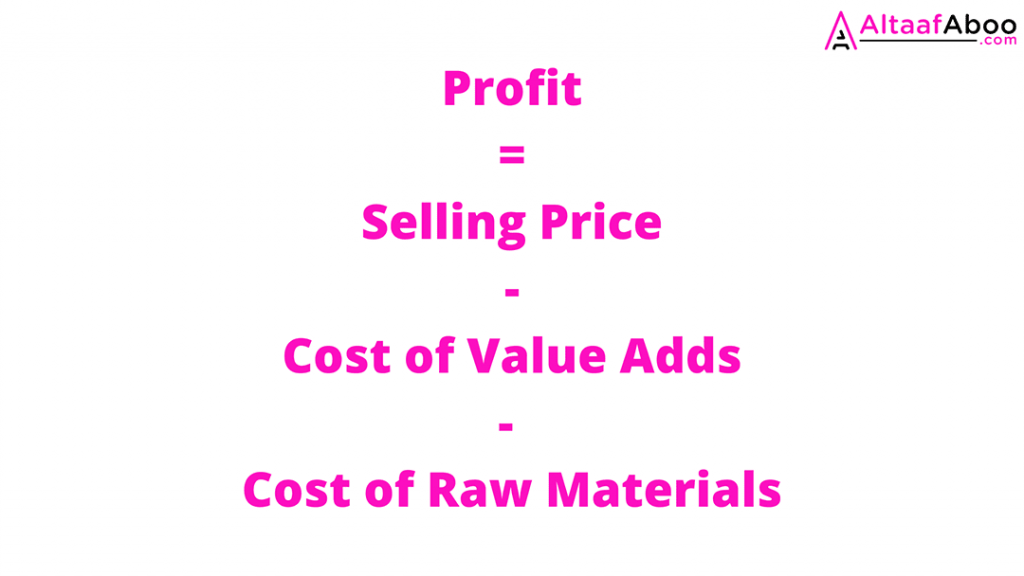

Customers are only willing to pay based on the value they get from your product.

There are two primary sources of value. One is the raw material and the other is the value you add.

Now your selling price can’t exceed the value that clients receive.

That creates this simple formula.

The raw material doesn’t mean something you dig up out of the ground like iron ore. It’s the cost of your input. If you have a convenience store than it’s the cost price of your milk.

Your value adds in the example of a convenience store would be your location and being open 24 hours a day. The cost of your value adds is what it costs you to provide that value. You’ll have to pay rent, and you’ll have to pay your staff overtime to work through the night. You may even need added security at these hours.

Your selling price can’t exceed the value that people receive from your product. The more value you add, the higher your selling price. If you want to increase your selling price, you need to add more value.

Your Customers Determine Value

If your convenience store is in the suburbs with traditional families, then they may not care to buy milk at 2 AM.

Looking back at the formula above. To become more profitable, you either need to reduce your costs or increase your selling price. If you are adding costs that your customers don’t value then you are reducing your profitability.

The costs of raw materials are usually fixed. It’s tough to produce something much cheaper in this competitive world.

Your secret lever is to add the most value at the least cost to yourself.

This applies to any business, but we’ll break down the example of the convenience store above.

The two key ways you are adding value:

1. You are closer than the store in the city

2. You are available 24 hours a day

Both of these value adds have a cost

1. Rent

2. Overtime salaries and added security

For these values you add, you charge a buck or two extra to your customer.

Your Customer is Happy to Pay for Value

They know that if they travelled to the large store in the city during the day and bought in bulk, they would pay less. Your customer sees this value add and is willing to pay for it.

They also put a price on this convenience. Your customer will only pay a buck or two extra. They are not willing to spend two or three times the amount for a carton of milk.

People needs to see more value in your convenience than it costs you to create that convenience.

Taking a look at our formula.

We’ll assume that the cost of milk is the same for all stores.

We have two options left to increase profits. We need to increase our selling price or reduce the cost of our value adds.

In the suburbs with traditional families, there may not be many people shopping at 2 AM. They shopping after and before they leave for work. There are also the stay at home parents who need one or two things between their big weekend shopping trips. Though, almost no-one is up in the middle of the night.

On a 24-hour cycle, you have three shifts of staff. Instead of being open 24 hours a day, you could close at 10 PM and reopen at 6 AM. Doing this may enable you to keep 99% of your customers while reducing your costs.

Because they never saw the value in buying milk at 2 AM, your offering was not profitable.

You’ll reduce your staff costs by a third or more and still provide 99% of the value you were providing.

Adding Value Almost Always Has a Cost

You need to ensure that your customer values that cost.

You can ask your customers if it’s better to remain open 24 hours or 18 hours a day. I’m sure you’ll find that everyone will choose 24 hours. The question you need to answer is how much are they willing to pay for those extra hours. If they are not willing to pay than you not adding real value.

The same goes for any industry, even an artist. If she purchases a canvas and some oil paints, then that’s the cost of her raw materials.

The cost of the canvas is 10 bucks, and the oil paint is another 10 bucks. The cost of her value add is her time. Suppose it takes 8 hours to produce a painting.

Let’s assume she has no other skills than being an artist. She would be earning 10 bucks per hour, flipping hamburgers, if she wasn’t painting.

Now we’ll add up the costs. 20 bucks of raw materials and 80 bucks worth of her time is a 100 bucks in total. If she can’t sell the painting for at least a 100 bucks than it would be more profitable for her to be flipping hamburgers.

She may not be happier, but she’ll be richer. This is the profit formula after all, not the happiness formula.

Though, she may be able to sell her painting for thousands, making it hugely profitable.

The question is, how can you add the value your customer wants at the lowest cost to yourself.

There are many ways to add value to your customer. Fast food outlets save you time at a price. Brands create their own clothing designs, sometimes at a very high price.

Some of these may only make a profit in the long term, while others are more immediate. The painter could get better over time, so even if she isn’t profitable right now, she could be in the future.

The More Unique Your Value Add, The Higher The Potential Selling Price

If you are the only 24-hour pharmacy within driving distance than you can charge a whole lot more than if there are a dozen 24-hour pharmacies around.

It’s also much harder for someone else to compete away your value add if it’s unique. No-one can create a Picasso but Picasso, but anyone who sees you making a fortune selling snacks at 2 AM can copy you.

If the only way to sell your product is at a loss, then there is something wrong with your formula. Perhaps no-one sees the value you add or even worse, the value you add is negative.

If the only reason people are willing to buy your product is at a loss to you, then your profit formula is broken. This is most likely because the cost of adding that value is more than what someone is willing to pay for it.

Looking at a tech example, Airbnb is a popular company that struggles with this formula. Allowing individuals to rent their private residences for the short term is valuable.

The only problem is that it currently costs them more to add that value than people are willing to pay for it. They will have to find a way to reduce their costs or increase their value if they want to remain profitable.

In the end, you need to tweak your formula based on what your customers not only want but are willing to pay for.